- EasyCard

- Trade

- Help

- Announcement

- Academy

- SWIFT Code

- Iban Number

- Referral

- Customer Service

- Blog

- Creator

Explaining TT Payment Rates and Their Impact on Currency Exchange

Image Source: unsplash

A telegraphic transfer is an electronic bank-to-bank transfer used for moving money across countries. You might see it called a t/t payment or a wire transfer. TT payment rates are the exchange rates banks use when you send or receive money through tt payments. These rates matter because they decide how much money you actually get or pay in an international payment. Even a small change in tt payment rates can mean you lose or gain a lot. By knowing the differences in tt payment rates, you can spot hidden fees and save money.

| Year | Number of Transfers Originated | Total Value of Transfers Originated (in $ millions) | Average Value per Transfer (in $ millions) |

|---|---|---|---|

| 2024 | 209,916,835 | 1,133,419,684 | 5.40 |

Key Takeaways

- TT payment rates include a hidden bank margin that affects how much money the recipient gets in international transfers.

- Banks charge fees and use different rates for sending and receiving money, so always check the exact rates and fees before you send.

- Intermediary banks can add extra fees and delays, so choose your transfer method carefully to avoid surprises.

- Comparing banks and alternative services can save you money and get better exchange rates for your transfers.

- Double-check recipient details and timing to avoid costly mistakes and get the best value from your telegraphic transfer.

TT Payment Rates Overview

Image Source: pexels

What Is a Telegraphic Transfer?

A telegraphic transfer lets you send money from your bank account to someone in another country. You start by giving your bank the recipient’s details, such as their name, account number, and the amount you want to send. Your bank then uses a secure network, like SWIFT, to send instructions to the recipient’s bank. Sometimes, intermediary banks help move the money if your bank does not have a direct connection. The recipient’s bank receives the instructions and credits the funds to the recipient’s account. This process usually takes 1 to 5 business days. You need to provide accurate information to avoid delays or extra fees. Many people and businesses use telegraphic transfers for international payments, including trade and personal remittances.

TT Payment Rates Explained

When you use telegraphic transfers, you deal with tt payment rates. These rates decide how much money the recipient gets after currency conversion. Banks set tt payment rates by starting with a base exchange rate, often called the mid-market rate. They then add a margin or markup to this rate. For example, a Hong Kong bank may take the mid-market rate for USD to EUR and add a margin of 0.05%. This margin is the bank’s profit. The final tt payment rate you see is the mid-market rate plus the bank’s margin. Each bank sets its own margin, and it can change based on the currency, the amount, or the transfer method. You may not always see the exact markup, but it affects the amount received in telegraphic transfers.

Tip: Always check the tt payment rates before sending money. Even a small difference in the rate can change the amount the recipient gets by hundreds of USD.

Buying vs. Selling Rates

Banks use different rates for telegraphic transfer buying and telegraphic transfer selling. The buying rate applies when you receive foreign currency into your local account, such as when someone sends you USD from abroad. The selling rate applies when you send money out in a foreign currency, like sending USD to Europe. Usually, the telegraphic transfer buying rate is lower than the selling rate because banks add a margin for their service. Here is a simple table to help you understand:

| Rate Type | When Used | Example (USD) |

|---|---|---|

| Buying Rate | Receiving foreign currency (inward telegraphic transfers) | You receive USD 1,000 from overseas |

| Selling Rate | Sending foreign currency (outward telegraphic transfers) | You send USD 1,000 to another country |

You should know which rate applies to your transaction. This helps you estimate the final amount in telegraphic transfers and avoid surprises.

How TT Payment Rates Affect International Payment

Bank Rate Setting

When you send money using telegraphic transfers, banks decide the exchange rate you get. Banks do not use the real-time market rate. Instead, they start with the interbank rate, which is the average rate banks use to trade currencies with each other. Banks then add a markup, usually between 4% and 6%. This markup helps banks earn a profit on each telegraphic transfer. For example, if the interbank rate for USD to EUR is 1.10, a Hong Kong bank might offer you a rate of 1.05. The difference between these rates is the bank’s margin. This margin changes based on the currency, the amount, and the bank’s own policies. You rarely see the true interbank rate when you make international transfers through banks. Services like Wise sometimes offer rates closer to the interbank rate, but most banks keep their rates higher to cover costs and make money.

Note: Always ask your bank for the exact telegraphic transfer rate before you confirm an international payment. This helps you understand how much you will actually pay or receive.

TT Rates vs. Market Rates

You might wonder why the rate you see online is different from the rate your bank gives you for telegraphic transfers. The answer lies in how banks set tt payment rates compared to market rates.

- TT rates are the actual rates banks use for telegraphic transfers and international wire transfer transactions.

- Market exchange rates, also called mid-market or interbank rates, show the real-time value of currencies based on supply and demand.

- Banks add a markup or fee to the market rate to create the tt payment rate you get.

- The mid-market rate is only a reference. You cannot use it directly for telegraphic transfers or international wire transfer payments.

- TT rates include extra costs, so they are less favorable than the pure market rate.

- When you use telegraphic transfers, you pay the bank’s rate, not the rate you see on financial news sites.

This difference means you often get less foreign currency than you expect when making cross-border payments. The markup covers the bank’s risk, costs, and profit. Some online services show you the mid-market rate and add a clear fee, but most banks include their fee in the telegraphic transfer rate itself.

Impact on Currency Received

The gap between the telegraphic transfer rate and the market rate affects the final amount you or your recipient gets. When you send money through telegraphic transfers, the bank’s spread or margin reduces the amount of foreign currency delivered. For example, if you send USD 1,000 to Europe using a telegraphic transfer, the recipient may get less than the market rate would suggest. The bank’s margin comes out of the total, so the more you send, the more you lose to the spread.

Tip: Even a small difference in the telegraphic transfer rate can cost you hundreds of USD on large international transfers. Always compare rates before you choose a provider for cross-border payments.

You should always check the telegraphic transfer rate and ask about any extra fees. This helps you avoid surprises and makes sure you get the best value for your international payment. If you use telegraphic transfers often, small savings on each transaction can add up over time. Understanding how banks set these rates gives you more control over your money when making international transfers or tt payments.

Fees and Costs in Telegraphic Transfers

Image Source: unsplash

Bank Fees and Intermediary Charges

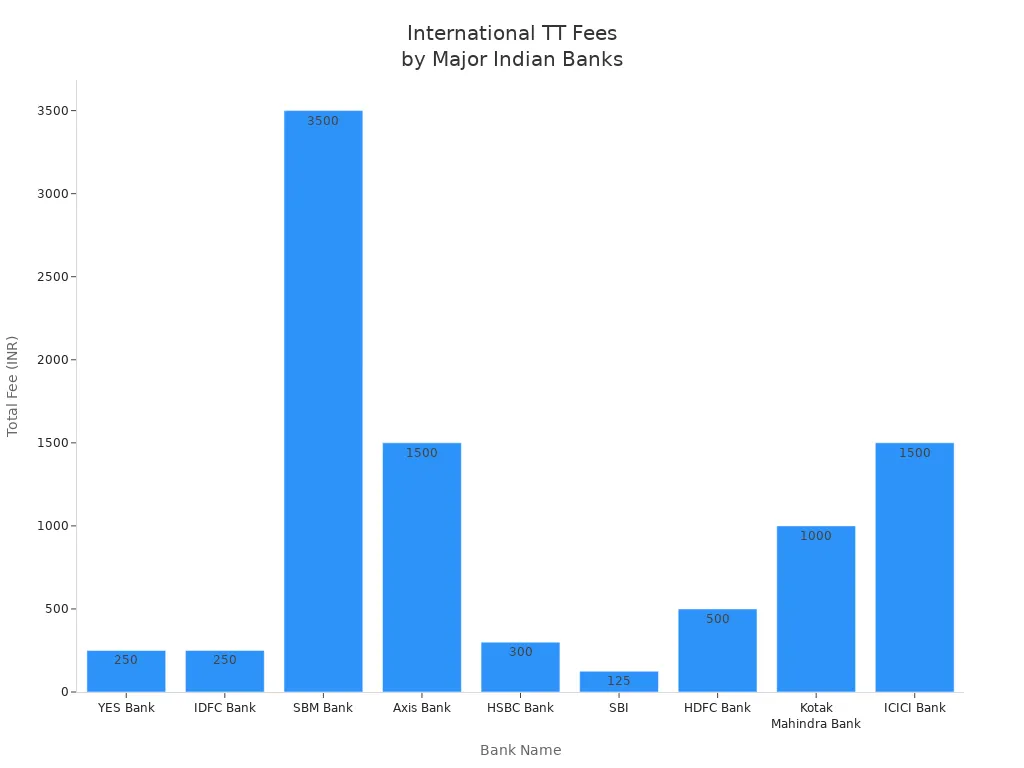

When you use a telegraphic transfer, you pay more than just the amount you send. Banks charge fees for processing telegraphic transfers, usually between $10 and $50 per transaction. If your bank does not have a direct link to the recipient’s bank, intermediary banks step in. These large international banks, such as Citibank or HSBC, help route your money through the SWIFT network. Each intermediary bank can add its own fee, often $15 to $30. The recipient’s bank may also charge a fee, usually up to $15. You may not know these charges in advance because they depend on the banks involved.

You can pay these fees in different ways:

- OUR: You pay all fees upfront, so the recipient gets the full amount.

- SHA: You and the recipient share the fees.

- BEN: The recipient pays all fees, which are deducted from the transfer.

If you send $10,000 using the BEN method and there is a $15 intermediary fee and a $15 beneficiary fee, the recipient receives $9,970.

| Bank Name | Typical Fee (USD) | Notes on Extra Charges |

|---|---|---|

| HSBC Bank | 0.5% (min $4, max $200) | Intermediary fees apply, GST extra |

| Citibank | $30 | Intermediary and receiver bank fees possible |

| HDFC Bank | $7–$15 | Additional intermediary bank fees may apply |

| ICICI Bank | $13–$20 | Fees vary by method and currency |

Intermediary banks act as middlemen in telegraphic transfers, and each one can add both cost and delay.

Flat Fees vs. Percentage Fees

Banks use two main types of fees for telegraphic transfers: flat fees and percentage-based fees. A flat fee means you pay the same amount no matter how much you send, such as $30 per telegraphic transfer. A percentage fee means you pay a part of the total amount, like 1% of what you send. Flat fees give you cost predictability, but they can be expensive for small transfers. Percentage fees scale with the amount, so they may cost more for large transfers unless the bank sets a maximum cap.

- Flat fees are better for large telegraphic transfers.

- Percentage fees may be cheaper for small amounts, but can add up for big transfers.

- Some banks cap percentage fees, making them more affordable for high-value telegraphic transfers.

- Online telegraphic transfers often have lower fees than those started at a bank branch.

Tip: Always check if your bank uses a flat fee or a percentage fee before you start a telegraphic transfer.

Processing Times and Extra Charges

Telegraphic transfers do not always arrive instantly. Most international telegraphic transfers take 1 to 5 business days. The time depends on bank cut-off times, weekends, holidays, and the number of intermediary banks involved. If you want your telegraphic transfer to arrive faster, you can pay extra for expedited service. Some banks offer same-day or next-day delivery for an additional fee.

- Domestic telegraphic transfers usually finish within 24 hours.

- International telegraphic transfers may take longer if there are many intermediary banks.

- Extra charges for amendments or cancellations are common. If you need to change or cancel a telegraphic transfer, expect to pay another fee, sometimes $20 or more.

- Double-check recipient details to avoid costly mistakes.

Paying more for expedited telegraphic transfers can speed up delivery, but always weigh the extra cost against your need for speed.

Factors Influencing TT Payment Rates

Exchange Rate Margins

When you send money using a telegraphic transfer, banks do not use the same rates you see online. Banks add a margin, or markup, to the interbank or mid-market rate. This margin is often hidden and can be the largest part of your total cost. Here is how exchange rate margins affect your telegraphic transfer:

- Banks apply a margin over the wholesale rate, which only large financial institutions can access.

- This margin usually ranges from 0.7% to 1.5%. For example, if you send $10,000, you might pay up to $150 just from the margin.

- Banks also charge transfer fees, sometimes between 3% and 5% of your transfer amount.

- Smaller transfers often have higher margins, so frequent small telegraphic transfers can cost you more.

- Extra fees, like intermediary bank charges or expedited service, add to your total cost.

You should always check the exchange rate margin before making a telegraphic transfer. Even a small difference in the margin can change the amount your recipient gets.

Market Fluctuations

Currency values change every day. These changes, called market fluctuations, affect the rate you get for a telegraphic transfer. If the value of your currency drops before your transfer goes through, your recipient will get less money. Some banks update their rates several times a day, while others set rates once each morning. Timing matters. If you send a telegraphic transfer when the market is unstable, you may lose money. Watching the market and choosing the right time can help you get a better rate.

Tip: Ask your bank when they set their telegraphic transfer rates. This helps you plan your transfer for the best possible outcome.

Bank Policies

Each bank sets its own rules for telegraphic transfer rates and fees. For example, Hong Kong banks may charge a flat fee of $30 for international transfers, while others include the service in a monthly account fee. Some banks use different clearing methods, which can affect how quickly your telegraphic transfer arrives and how much it costs. You may also see differences in safety checks and processing times. Because there is no standard policy, you should always compare banks before choosing where to send your telegraphic transfer.

- Fees for telegraphic transfers can vary, even for the same amount.

- Some banks offer bundled services, which may lower your effective cost.

- Processing and safety policies differ, so always ask about the details.

Understanding these factors helps you make smarter choices and avoid paying more than you need for a telegraphic transfer.

Getting the Best TT Payment Rate

Comparing Providers

You can save money on a telegraphic transfer by comparing different banks and money transfer providers. Start by checking the exchange rates each provider offers. Even a small difference in the rate can change how much your recipient gets. Look at all the fees, including those for sending and receiving. Some banks add hidden charges, so ask for a full breakdown. Use online comparison tools to see real-time rates, fees, and transfer speeds. Check reviews on social media and forums to learn about customer service and reliability. Make sure you know how long the telegraphic transfer will take, especially if you need the money to arrive quickly.

Tip: Always ask if there are extra charges for amendments or cancellations before you send a telegraphic transfer.

Negotiating Fees

You can often lower your telegraphic transfer fees by negotiating with your bank or provider. Show them that you know what other banks charge for international transfers. If you send money often or in large amounts, ask for a discount. Banks may offer better rates if you bundle services or show loyalty. Prepare by knowing your current fees and how much you transfer each month. Focus on negotiating electronic transaction fees, which usually have higher margins. If you use a branch, ask if online telegraphic transfer services are cheaper.

- Show your payment history to prove you are a valuable customer.

- Compare offers from several providers to get the best deal.

- Bundle services to get lower fees.

Using Alternative Services

You do not have to use a traditional bank for every telegraphic transfer. Many alternative services offer better rates and lower fees for international wire transfer payments. For example, Wise uses the mid-market rate and charges low, clear fees. Remitly lets you choose between fast or low-cost options. Western Union gives you cash pickup choices. XE and OFX help with large telegraphic transfers and offer rate alerts. These services often move money faster and cost less than banks.

| Provider | Exchange Rate Type | Typical Fee (USD) | Speed | Special Features |

|---|---|---|---|---|

| Wise | Mid-market | Low, transparent | 1-2 days | Real-time rate, low markup |

| Western Union | Own rate | Varies | Minutes-hours | Cash pickup, global reach |

| Remitly | Own rate | Low to moderate | Minutes-3 days | Economy/Express options |

| XE | Competitive | No fee | 1-3 days | Rate alerts, large transfers |

If you send a telegraphic transfer of USD 5,000, a bank may charge USD 50 in fees and use a less favorable rate, while Wise may charge USD 20 and use a better rate. This means your recipient could get up to USD 100 more with an alternative provider. Always compare before you choose, especially for cross-border payments.

Understanding tt payment rates and telegraphic transfer fees helps you avoid unnecessary costs in international payments. When you know the types of fees and how they vary, you can choose the most cost-effective method.

- Use real-time tools like FX rate calculators to compare rates and fees.

- Consider alternative services for better rates and lower charges.

To make smarter payments:

- Compare providers and check all fees.

- Double-check recipient details to prevent costly mistakes.

- Time your transfers to avoid delays and extra charges.

Staying informed lets you keep more of your money when sending funds abroad.

FAQ

What is the difference between a TT payment rate and the rate I see online?

Banks set TT payment rates with a margin above the mid-market rate you see online. You usually get less foreign currency than the online rate suggests. Always check your bank’s actual TT payment rate before sending money.

Why do Hong Kong banks charge different fees for TT payments?

Each Hong Kong bank sets its own fee structure. Some use flat fees, while others use percentage-based fees. Intermediary banks may add extra charges. Always ask for a full breakdown of all fees before you make a transfer.

How long does a telegraphic transfer take to reach the recipient?

Most international TT payments arrive in 1 to 5 business days. The time depends on the banks involved, the number of intermediary banks, and the destination country. Delays can happen if you enter incorrect details.

Can I cancel or change a TT payment after sending it?

You can request a cancellation or amendment, but banks may charge extra fees. The process can take several days. Always double-check recipient details before confirming your transfer to avoid costly mistakes.

Are online TT payments cheaper than branch transfers?

Online TT payments often have lower fees than branch-initiated transfers. Some Hong Kong banks offer special rates for online services. Compare both options to find the best deal for your international payment.

Telegraphic transfers (TT) streamline international payments but often come with high fees ($10-$50) and exchange rate markups (4%-6%), reducing the amount received. To maximize value in 2025, pair TTs with BiyaPay. BiyaPay offers transfer fees as low as 0.5%, significantly less than traditional bank charges, with real-time exchange rate transparency across 30+ fiat currencies and 200+ cryptocurrencies in 100+ countries. Its Biya EasyCard, a virtual card with no annual fee, supports Amazon, eBay, and PayPal, enabling seamless payments in 190+ countries for suppliers or personal transactions. Whether paying overseas vendors or sending remittances, BiyaPay ensures same-day transfers and simple setup with ID verification. Licensed in the U.S. and New Zealand, it guarantees secure, compliant transactions. Optimize your TT payments with BiyaPay’s cost-effective, transparent platform. Sign up at BiyaPay today to save on international transfers!

*This article is provided for general information purposes and does not constitute legal, tax or other professional advice from BiyaPay or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional.

We make no representations, warranties or warranties, express or implied, as to the accuracy, completeness or timeliness of the contents of this publication.

Contact Us

Company and Team

BiyaPay Products

Customer Services

is a broker-dealer registered with the U.S. Securities and Exchange Commission (SEC) (No.: 802-127417), member of the Financial Industry Regulatory Authority (FINRA) (CRD: 325027), member of the Securities Investor Protection Corporation (SIPC), and regulated by FINRA and SEC.

registered with the US Financial Crimes Enforcement Network (FinCEN), as a Money Services Business (MSB), registration number: 31000218637349, and regulated by FinCEN.

registered as Financial Service Provider (FSP number: FSP1007221) in New Zealand, and is a member of the Financial Dispute Resolution Scheme, a New Zealand independent dispute resolution service provider.