- EasyCard

- Trade

- Help

- Announcement

- Academy

- SWIFT Code

- Iban Number

- Referral

- Customer Service

- Blog

- Creator

Statrys vs. Traditional Banks for Enterprise Cross-Border Remittances: Which Is Better for Chinese Businesses?

Image Source: unsplash

Statrys is suitable for small and medium-sized enterprises (SMEs) prioritizing convenient account opening, transparent fees, and fast transfer speeds, while traditional banks like Hong Kong banks are better suited for large enterprises with high demands for fund security and exchange rate risk management. Chinese businesses, when choosing enterprise cross-border remittance solutions, focus most on exchange rate fluctuations, transfer timing, fee costs, payment security, and fund liquidity. Businesses can align their needs to select the optimal solution.

Key Points

- Statrys offers fully online account opening and fast transfers, suitable for SMEs seeking efficiency and low costs.

- Traditional banks have complex procedures, high fees, and longer transfer times, better suited for large enterprises with high demands for fund security and compliance.

- Statrys provides transparent fees with currency conversion costs as low as 0.4%, significantly reducing cross-border remittance costs for businesses.

- Statrys supports 11 major currencies, enabling flexible multi-currency fund management and improving liquidity.

- Businesses should choose Statrys or traditional banks for cross-border remittances based on their scale, funding needs, and risk preferences.

Service Models

Statrys Model

Statrys adopts a fully digital enterprise cross-border remittance service model. Businesses can initiate transfers through an online platform without visiting physical branches. The system automates transfer instructions, intelligently identifies recipient information, and reduces manual intervention. The Statrys platform supports multi-currency account management, allowing businesses to perform foreign currency exchanges anytime to meet international business needs flexibly. The platform interface is clean, with a clear operational process, enabling businesses to track transfer progress in real-time. Statrys also provides automated reconciliation and transaction record export functions for convenient financial management. The digital process significantly shortens transfer times, enhancing fund flow efficiency. The Statrys model is ideal for SMEs seeking high efficiency, low costs, and flexible operations, particularly in scenarios with frequent cross-border remittances and diverse currencies.

Traditional Bank Model

Enterprise cross-border remittance services from traditional banks, such as Hong Kong banks, rely on offline processes and multi-level intermediaries. Businesses must visit bank branches to submit transfer applications and prepare relevant documentation. Banks review the source and purpose of funds to ensure compliance. Transfer methods vary, including wire transfers (T/T), Western Union, MoneyGram, and Hong Kong offshore company accounts. For wire transfers, businesses pay first and ship later, with banks processing through the SWIFT system via multiple intermediaries, with transfer times affected by holidays and time differences. Traditional banks impose transfer amount restrictions, with amounts exceeding certain thresholds subject to scrutiny by tax and foreign exchange authorities. Businesses must also comply with relevant national laws and international regulations to prevent risks like money laundering. The traditional bank model involves complex procedures, high fees, and longer transfer times, suitable for large enterprises with stringent requirements for fund security and compliance.

Tip: When choosing enterprise cross-border remittance services, businesses should fully consider their scale, operational convenience, and compliance risks to match the appropriate service model.

Account Opening Process

Statrys Account Opening

Statrys provides a fully online account opening service for businesses. Businesses only need to schedule an account opening time through the platform and submit basic documents, with the system conducting a preliminary review. Subsequently, businesses can remotely upload required materials without visiting physical branches. The entire account opening process typically completes within 3-5 business days, with 85% of businesses able to open accounts successfully within 3 days. Statrys does not charge account opening fees or require a minimum deposit. Businesses can apply anytime, anywhere, with the registration process taking just 5 minutes. The platform supports multi-currency accounts in 11 foreign currencies, facilitating international payments and receipts. Statrys also provides virtual and physical Mastercard options, enabling businesses to manage employee expenses and improve financial efficiency. Oversight by Hong Kong customs and relevant licenses ensure account security, enhancing businesses’ confidence in fund safety.

Bank Account Opening

The account opening process for enterprise accounts at Hong Kong banks is relatively complex. Businesses need to prepare business licenses, legal representative identity documents, and company articles of association. Banks assign personnel to verify the authenticity and completeness of documents and conduct due diligence. Some banks offer dedicated enterprise account opening counters to assist with filling out information, organizing documents, and ongoing maintenance. In some regions, “one-stop enterprise establishment service counters” integrate business registration, seal production, bank account opening, and tax registration, completing all procedures as quickly as one day. Banks also promote account opening standards and waive certain fees to enhance convenience. However, in most cases, businesses must visit branches, and the account opening period can extend to weeks if documents are incomplete or reviews are stringent.

Convenience Comparison

Statrys’ online account opening process significantly enhances convenience. Businesses can complete all steps remotely without visiting branches, saving substantial time and labor costs. With no minimum deposit or account opening fees, it’s ideal for SMEs looking to quickly start international operations. While some Hong Kong bank branches offer one-stop services and fast-track channels, the overall process relies on offline operations, with multiple document reviews and due diligence steps, leading to longer account opening periods. For businesses prioritizing efficiency and flexibility, Statrys’ account opening experience is more appealing.

Enterprise Cross-Border Remittance Fees

Image Source: pexels

Statrys Fees

Statrys offers a highly competitive fee structure for enterprise cross-border remittances. Businesses using the Statrys platform benefit from currency conversion fees as low as 0.4% for major currencies, starting at 0.6% for non-major currencies. International transfer receipt fees start at $7.7, and payment fees start at $10.9. Statrys uses real-time mid-market exchange rates, with conversion costs significantly lower than Hong Kong banks. Account opening and monthly management are free, with an $11.3 management fee only applied when fewer than 5 outbound transfers are made monthly. Businesses face no minimum deposit or maximum transaction limits, ideal for SMEs with frequent cross-border remittances. Statrys also provides virtual and physical Mastercard cards, with a 1.5% conversion fee for non-HKD transactions and a 1.99% additional fee for designated ATM withdrawals. Overall, Statrys significantly reduces international payment costs for businesses.

| Fee Category | Details |

|---|---|

| Transfer Fees | Major currency conversion fees as low as 0.4%, non-major currencies from 0.6%; international transfer receipt minimum $7.7, payment minimum $10.9 (agent banks may charge additional fees) |

| Exchange Rate Benefits | Real-time mid-market exchange rates, conversion fees as low as 0.4%, more favorable than Hong Kong banks |

| Account Fees | No opening fees, no monthly fees (except $11.3 for fewer than 5 monthly outbound transfers) |

| Transaction Limits | No minimum deposit or maximum transaction caps, suitable for frequent transfers |

| Mastercard-Related Fees | 1.5% conversion fee for non-HKD transactions, 1.99% additional fee for designated ATM withdrawals |

Businesses only need to log into their Statrys business account, select the “transfer” function, and enter transfer details to view real-time exchange rates and fees. The process is transparent and efficient. After submission, the system sends a confirmation email with a tracking number and estimated arrival time, enabling businesses to monitor fund movements.

Bank Fees

Hong Kong banks’ fees for enterprise cross-border remittances are generally higher than Statrys’. Handling fees typically range from 0.5% to 3% of the transaction amount, with a minimum of about $10 per transfer and a maximum of up to $150. Cross-border wire transfers also incur SWIFT fees, usually $10 to $50. Agent banks may charge an additional $20 to $100. For a $5 million cross-border transfer, total costs, including all fees, could range from $20,000 to $150,000. Hong Kong banks typically mark up exchange rates by 1% to 3%, with spreads ranging from 0.1% to 2%. These hidden costs result in actual foreign exchange expenses far exceeding the mid-market rate. Multiple intermediaries in the settlement process extend transfer times, keeping overall transaction costs high.

| Fee Type | Fee Range/Ratio | Description and Example |

|---|---|---|

| Handling Fees | 0.5% - 3% | Charged as a percentage of the transaction amount, minimum $10, maximum $150 per transfer |

| SWIFT Fees | $10 - $50 | Fixed fees for cross-border wire transfers |

| Agent Bank Fees | $20 - $100 | Additional charges by agent banks |

| Total Cost Estimate | $20,000 - $150,000 | For a $5 million transaction, including all fees |

| Exchange Rate Markup | 1% - 3% | Banks add markups to exchange rates, with spreads of 0.1% - 2% |

| Settlement Time | 1 - 3 days | Multiple intermediaries involved, extending transfer times |

Hong Kong banks’ exchange rate markups and multiple handling fees result in businesses bearing costs far higher than apparent fees. Businesses should thoroughly understand all fee details in advance to avoid budget overruns due to hidden costs.

Fee Transparency

Statrys excels in fee transparency. When initiating a transfer, the system displays all related fees and exchange rates in real-time, ensuring businesses clearly understand every expense. All fees are explicitly listed on the operation page, eliminating concerns about hidden costs. After completing a transfer, businesses can export detailed transaction records through the platform, facilitating financial reconciliation and compliance audits.

In contrast, Hong Kong banks’ fee structures are more complex. Businesses often need to separately understand handling fees, SWIFT fees, agent bank fees, and exchange rate markups. Some fees only become apparent during the transfer process, making it difficult for businesses to grasp total costs upfront. Exchange rate markups are a hidden cost, often resulting in higher-than-expected payments. Fee details are scattered across different stages, increasing financial management complexity.

Tip: When choosing enterprise cross-border remittance channels, businesses should prioritize platforms with transparent fee structures to avoid impacts from hidden costs on financial planning.

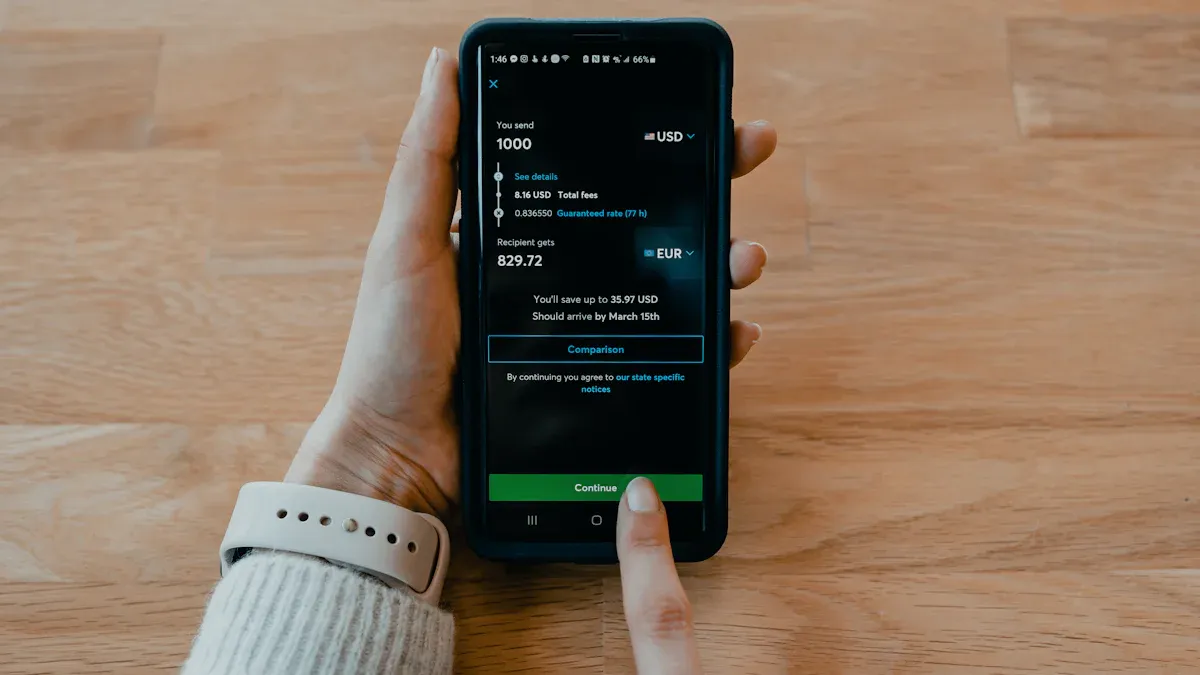

Transfer Speed

Image Source: unsplash

Statrys Transfer Speed

Statrys offers highly competitive transfer speeds for enterprise cross-border remittances. After initiating a transfer through the Statrys platform, the system automatically identifies recipient information and completes compliance reviews. Data shows that over 60% of transfers are completed within 20 seconds. Statrys uses advanced digital clearing systems, significantly reducing the waiting time of traditional cross-border payments. Businesses do not need to wait for multi-level intermediaries, with funds reaching recipient accounts in seconds. The Statrys platform also supports real-time transfer tracking, allowing businesses to monitor fund movements anytime. For trading companies and cross-border e-commerce needing quick settlements, Statrys’ near-instant transfer capability significantly enhances fund turnover efficiency, helping businesses seize international market opportunities.

Bank Transfer Speed

Hong Kong banks’ transfer speeds for enterprise cross-border remittances lag behind. Transfers initiated through bank counters typically require 1-2 business days to process, with actual arrival times of 3-5 business days. Online channels like internet banking or mobile apps can send funds the next business day after review, with the fastest transfers arriving in 24 hours, but most take 3-7 business days. Bank of China’s electronic banking channels can achieve 24-hour arrivals when information is accurate, but may take up to a week otherwise. Overall cross-border transfer cycles typically range from 1-5 business days. Transfer speed is affected by factors like time differences, holidays, intermediary banks, and recipient bank processing efficiency. During peak periods or international holidays, fund arrival times may be further delayed.

| Transfer Channel | Estimated Arrival Time | Influencing Factors and Notes |

|---|---|---|

| Counter-Initiated | 1-2 business days for processing, 3-5 business days for arrival | Affected by time differences and holidays; arrival time depends on the recipient bank’s processing speed. |

| Online Channels (Internet/Mobile Banking) | Sent the next business day after review, fastest 24 hours, typically 3-7 business days | Depends on intermediary and recipient bank processing speeds; accurate information enables faster arrivals, while intermediary banks may extend times. |

| Bank of China Electronic Banking | Sent the next business day, fastest 24 hours, slowest about one week | Faster processing with accurate information; intermediary banks affect arrival times. |

| Overall Cross-Border Transfers | Typically 1-5 business days | Weekends and holidays extend arrival times; varies by bank. |

Speed Comparison

The difference in transfer speed between Statrys and Hong Kong banks is stark. Statrys leverages a digital clearing network, with over 60% of cross-border remittances arriving within 20 seconds, greatly enhancing business fund liquidity. Real-world data from the Hong Kong Monetary Authority shows that JD-HKD cross-border settlements reduced from 2-3 days with traditional SWIFT systems to 10 seconds, highlighting the advantage of modern digital platforms. Statrys’ statistics indicate that same-currency payments using traditional SWIFT systems have far longer processing times than the Statrys platform. Hong Kong banks rely on SWIFT and intermediary banks, requiring multi-level transfers, with arrival cycles of 1-5 business days, extended further by holidays or incomplete information.

Statrys’ transfer speed brings multiple benefits to businesses. It enables rapid international settlements, improving fund turnover efficiency and reducing opportunity costs from delayed arrivals. For trading companies and cross-border e-commerce, timely arrivals enhance customer satisfaction and partner trust. While Hong Kong banks excel in fund security and compliance, they cannot compete with Statrys in transfer speed. Businesses should choose cross-border remittance channels based on their needs for transfer timing.

Currency and Account Management

Multi-Currency Support

Statrys provides multi-currency accounts, supporting 11 major currencies, including HKD, USD, EUR, and RMB. Businesses can manage multiple currencies within a single account, eliminating the need for frequent account openings. Statrys offers 24-hour currency exchange services, allowing businesses to convert funds anytime based on needs. Conversion fees are as low as 0.4%, using real-time mid-market exchange rates, helping businesses save on forex costs. Accounts have no minimum deposit or maximum transaction limits, making cross-border remittances more flexible. Through the Statrys platform, businesses can:

- Easily manage multi-currency funds, reducing conversion frequency and costs

- Quickly open accounts, with 85% of businesses completing within 3 days

- Enjoy no opening or monthly fees (except for low-frequency transfers)

- Use virtual and physical Mastercard cards for efficient daily expense management

- Improve fund flow efficiency, with local transfers arriving same-day and international transfers in 2-3 business days

These services give businesses greater fund allocation capabilities in global markets, enhancing the efficiency and flexibility of cross-border remittances.

Account Flexibility

Hong Kong banks have limitations in currency support and account management. Businesses typically can only choose from a limited set of currencies like USD, EUR, GBP, and HKD, which may not meet all international business needs. Account management processes are cumbersome, often requiring businesses to:

- Open separate accounts for currencies like RMB and USD, increasing complexity and costs

- Provide company registration certificates, tax numbers, and valid registration addresses, with high account opening thresholds requiring local registration

- Deal with traditional account management models lacking integrated local and foreign currency management, resulting in low fund transfer efficiency

- Navigate complex procedures for cross-border fund operations, impacting fund usability

These limitations make cross-border remittance operations complex and reduce fund management flexibility. In contrast, Statrys’ multi-currency accounts and flexible management model are better suited for Chinese businesses seeking efficiency and convenience.

Security and Compliance

Statrys Security

Statrys places high importance on the security and compliance of enterprise cross-border remittances. The platform employs multi-factor authentication and encryption technologies to protect business account information and transaction data. Every transfer undergoes automated compliance reviews, with the system monitoring for abnormal transactions in real-time and issuing risk alerts. Statrys holds relevant Hong Kong financial licenses and is regulated by Hong Kong customs, ensuring all business processes comply with laws and regulations. The platform regularly updates security policies to prevent cyberattacks and data breaches. Businesses can view account activity in real-time through the platform and export detailed transaction records for compliance audits. Through these measures, Statrys creates a secure and transparent cross-border remittance environment for businesses.

Bank Security

Hong Kong banks have a robust security and compliance system for enterprise cross-border remittances. Banks ensure fund security and compliant operations through:

- Strict enforcement of anti-money laundering, anti-telecom fraud, cybersecurity, and data protection requirements to secure cross-border remittances.

- Leveraging advanced IT and data networks to assist businesses in conducting background checks and risk assessments on overseas partners, reducing collaboration risks.

- Complying with domestic and international laws on credit information, personal data, trade secrets, cybersecurity, and data protection to ensure compliant operations.

- Establishing supply chain finance compliance systems to verify transaction authenticity, fund flows, document flows, and goods flows, preventing fraudulent trade and fund cycling.

- Adhering to market entry regulations and business product oversight to prevent systemic risks and protect business and client interests.

- Policy banks providing low-cost funds and credit support, while addressing compliance requirements like overseas loan filings, cross-border guarantee registrations, exchange rate risk warnings, and arbitrage risk prevention.

These measures establish a solid foundation for Hong Kong banks in ensuring enterprise cross-border remittance security, compliance, and risk control. Businesses should fully assess their security and compliance needs when choosing remittance channels to match the appropriate service platform.

Customer Service

Statrys Service

Statrys focuses on providing efficient and flexible customer service for SMEs. The platform simplifies account opening and cross-border remittance processes through digital means. Key service features include:

- Offering enterprise account opening, cross-border payments, multi-currency accounts, and company cards, with a convenient process where 85% of businesses can open accounts within 3 days.

- Supporting businesses registered in Hong Kong, Singapore, and the British Virgin Islands, with no account opening fees or monthly fees (except $11.3 for fewer than 5 monthly outbound transfers).

- Multi-currency accounts supporting 11 major currencies, with exchange rates as low as 0.4%, no minimum deposit or maximum transaction limits, enabling flexible international transfers and lower conversion costs.

- Providing virtual and physical Mastercard cards for convenient employee expense management, with fees for non-HKD transactions and withdrawals.

- Supporting local transfers (FPS and CHATS) and international wire transfers (SWIFT and local currencies), with lower fees than Hong Kong banks and fast transfer speeds, ideal for SMEs with frequent international transactions.

- Regulated by Hong Kong customs with a Money Service Operator license, ensuring client fund safety.

Statrys provides one-on-one consultation and issue resolution through online customer service and dedicated account managers. Businesses can access operational guidance and real-time support anytime, enhancing the overall service experience.

Bank Service

Hong Kong banks offer mature and stable customer service for enterprise cross-border remittances. Banks primarily complete cross-border payments via wire transfers (Telegraphic Transfer) using the SWIFT system, which provides secure, reliable, and standardized communication. Businesses only need to provide sender and recipient account information, making the process relatively straightforward. Bank service processes are fixed and risk-controlled, suitable for large enterprises handling significant trade settlements.

Banks continuously innovate international services, introducing supply chain finance, blockchain-based cross-border payments, and personalized solutions. However, the overall service model remains focused on basic operations, with significant service homogenization, struggling to meet the personalized needs of SMEs and cross-border e-commerce. Businesses often face high costs, long cycles, and insufficient transparency in cross-border payment processes. SMEs and e-commerce sellers have limited service experiences in account opening, fund flows, and compliance.

Expert Advice: SMEs seeking efficient, flexible, and low-cost customer service should prioritize digital platforms like Statrys. Large enterprises with higher demands for fund security and compliance benefit more from Hong Kong banks’ standardized services.

Suitable Business Types

Trading Companies

Trading companies frequently settle funds in global markets, with high demands for transfer speed and exchange rate costs. Statrys provides multi-currency accounts and real-time exchange rates, enabling flexible management of international payments and receipts. Hong Kong banks excel in compliance and fund security, suitable for large-scale trade and long-term partnerships. Businesses should choose cross-border remittance channels based on their scale and transaction frequency.

Cross-Border E-Commerce

Cross-border e-commerce businesses prioritize account opening speed, account management, and cost control. Digital banks like Statrys offer clear advantages:

- Video verification replaces traditional in-person visits, shortening account opening to 3-7 days, much faster than Hong Kong banks.

- Licensed institutions provide bank pre-approval services, with a 92% account opening success rate compared to about 35% for Hong Kong banks.

- Statrys has no minimum deposit requirement, while Hong Kong banks like Mauritius ABC Bank require a minimum deposit of $50,000.

- Multi-currency management reduces exchange rate losses.

These features make Statrys more suitable for cross-border e-commerce businesses’ funding operations and remittance needs.

Small and Medium Enterprises

Statrys offers low fees, favorable exchange rates, and fast transfers, ideal for SMEs with frequent international transactions. SMEs can save on cross-border remittance costs and improve fund flow efficiency through Statrys. Hong Kong banks provide loans, investments, and comprehensive financial services, suitable for SMEs needing diverse financial products. SMEs should choose platforms based on their business priorities.

Large Enterprises

Large enterprises have higher demands for fund security, compliance, and large transaction assurances. Hong Kong banks, with robust risk control systems and international reputations, are the preferred choice. Banks offer comprehensive financial services, including supply chain finance, forex hedging, and large-scale fund settlements. Statrys suits large enterprises needing flexibility and cost control, particularly excelling in multi-currency management and fast transfers.

Selection Recommendations

Scenario Summary

Statrys and Hong Kong banks each have strengths in enterprise cross-border remittances. Statrys, with its digital platform, is ideal for SMEs seeking efficiency, low costs, and flexible operations. It supports multi-currency accounts, offers fast transfer speeds, and transparent fees, particularly suitable for small, high-frequency transactions and cross-border e-commerce. Hong Kong banks excel in fund security, compliance management, and large transaction assurances, providing supply chain finance, risk management, and tailored financial services for large enterprises and trading companies. Some banks enhance cross-border payment efficiency and security through fintech innovations like blockchain, reducing transaction costs. Businesses can choose the service model best suited to their scale, transaction frequency, and risk preferences.

Decision Factors

Chinese businesses choosing between Statrys and Hong Kong banks for cross-border remittances should focus on:

- Cross-Border Payment Efficiency and Transfer Timing: Statrys achieves minute-level transfers, improving fund utilization efficiency, while Hong Kong banks have complex procedures and longer cycles.

- Cost Control: Statrys’ fees are as low as 0.4%, compared to Hong Kong banks’ fees often exceeding 3%, suitable for large, low-frequency transactions.

- Compliance and Risk Management: Platforms must have robust anti-money laundering and data protection capabilities to ensure fund security and prevent account closures.

- Exchange Rate Management and Settlement Efficiency: Quality platforms offer fast settlements and tailored forex services to minimize exchange losses.

- Payment Network Coverage and Multi-Currency Support: Statrys supports 11 major currencies, facilitating global market expansion, while Hong Kong banks offer limited currency options, suitable for traditional trade settlements.

- Technological Empowerment and User Experience: Statrys integrates with major cross-border e-commerce platforms for automated accounting and convenient operations, while Hong Kong banks focus on standardized processes, ideal for businesses needing comprehensive financial services.

Expert Advice: Businesses should evaluate platforms’ service capabilities and cost structures based on their scenarios, transaction scale, and compliance needs to select the most suitable cross-border remittance solution.

Statrys excels with its digital, low-cost, and efficient services, ideal for SMEs seeking flexible operations. Hong Kong banks meet large enterprises’ needs with robust compliance and fund security. Chinese businesses should consider multi-currency collections, transfer timing, compliance risk control, technological empowerment, and localized services based on their business characteristics to choose the optimal cross-border payment solution.

FAQ

Which Currencies Does Statrys’ Enterprise Account Support?

Statrys’ enterprise account supports 11 major currencies, including USD, HKD, EUR, and RMB. Businesses can flexibly manage multi-currency funds within a single account to meet international business needs.

How Do Statrys and Hong Kong Banks Differ in Transfer Speed?

Over 60% of Statrys’ transfers arrive within 20 seconds. Hong Kong banks typically take 1-5 business days, significantly affected by intermediary banks and holidays.

What Documents Are Needed to Open a Statrys Account?

Businesses need to prepare business licenses, company articles of association, and legal representative identity documents. All materials can be uploaded online, making the process efficient and convenient.

How Are Statrys’ Transfer Fees Calculated?

Statrys’ major currency conversion fees are as low as 0.4%, with non-major currencies starting at 0.6%. International transfer fees start at $7.7 (USD), with a transparent fee structure businesses can check in real-time.

Does Statrys Meet Compliance and Security Requirements?

Statrys holds relevant Hong Kong financial licenses and is regulated by Hong Kong customs. The platform uses multi-layer encryption and automated compliance reviews to ensure business fund security and transaction compliance.

After a detailed comparison of Statrys and traditional banks for corporate cross-border remittances, it’s clear that each has its strengths. Statrys is an ideal solution for small and medium-sized enterprises and e-commerce businesses due to its efficiency, low cost, and flexibility. Traditional banks, on the other hand, continue to serve traditional businesses with large transaction needs due to their emphasis on fund security and compliance. No matter which option you choose, you may still encounter issues like complex procedures and opaque exchange rates. BiyaPay was created to solve this pain point, offering a more efficient and transparent cross-border financial solution. We support the conversion between various fiat and digital currencies, allowing you to easily complete global remittances with a remittance fee as low as 0.5% and same-day delivery. You don’t need a complex overseas bank account to invest in both U.S. and Hong Kong stocks on one platform, and you can use our real-time exchange rate query to seize the best conversion opportunities. Say goodbye to the hassle of traditional remittances, and register with BiyaPay today to start your smart investment journey.

*This article is provided for general information purposes and does not constitute legal, tax or other professional advice from BiyaPay or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional.

We make no representations, warranties or warranties, express or implied, as to the accuracy, completeness or timeliness of the contents of this publication.

Contact Us

Company and Team

BiyaPay Products

Customer Services

is a broker-dealer registered with the U.S. Securities and Exchange Commission (SEC) (No.: 802-127417), member of the Financial Industry Regulatory Authority (FINRA) (CRD: 325027), member of the Securities Investor Protection Corporation (SIPC), and regulated by FINRA and SEC.

registered with the US Financial Crimes Enforcement Network (FinCEN), as a Money Services Business (MSB), registration number: 31000218637349, and regulated by FinCEN.

registered as Financial Service Provider (FSP number: FSP1007221) in New Zealand, and is a member of the Financial Dispute Resolution Scheme, a New Zealand independent dispute resolution service provider.