- EasyCard

- Trade

- Help

- Announcement

- Academy

- SWIFT Code

- Iban Number

- Referral

- Customer Service

- Blog

- Creator

The Potential for Nvidia's Market Cap to Exceed $10 Trillion: It's Time to Increase Positions in 2025!

Warren Buffett once pointed out: “If a person makes a few correct decisions in his life and avoids major mistakes, the probability of his investment success will be greatly increased.” For most investors, although this sounds simple, it is full of challenges to actually implement.

Currently, we are looking at all the top stocks and trying to predict which stocks will perform outstandingly in 2025. Although we haven’t found a clear answer yet, if we change the question to “Which company will become the first in the world with a market cap exceeding $10 trillion”, we may get a clearer direction.

For now, Nvidia (NVDA) is undoubtedly the strongest contender to enter the “$10 trillion super list”.

Three Reasons for Nvidia’s Future Growth

Nvidia currently holds a leading position in the field of Graphics Processing Units (GPU), and the GPUs it produces play a crucial role in supporting the construction of AI servers and data centers. This trend is called the AI chip gold rush.

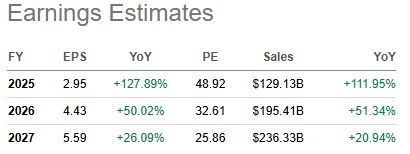

In the past two years, Nvidia’s stock price has increased by more than 900%, and this growth mainly comes from its GPU business. Especially in the past three years, the annual average growth rate of GPU revenue has exceeded 67%. It is expected that by 2025, Nvidia’s GPU revenue will reach $129 billion.

However, the real question is: Can Nvidia’s growth continue to maintain in the next few years?

The answer to this question largely depends on the development direction of artificial intelligence in the next decade. The following is a consensus report from the investment analysis platform SA:

According to SA’s forecast, Nvidia’s revenue growth will remain strong in the next few years, and the average annual growth rate is expected to reach 20.94% by 2027. This forecast may seem relatively conservative, especially considering Nvidia’s performance in the past decade. In the past five years, Nvidia’s compound annual growth rate was 62.43%, and in the past ten years, it was 37.84%.

Considering the current driving force of the AI revolution and the fact that the AI boom has just begun, it is very likely that Nvidia’s performance in the next few years will not be inferior to this.

Although some voices have pointed out that the future development of artificial intelligence is still uncertain and it is difficult to predict how the demand for GPUs will change, there are still several key factors that can strongly support Nvidia’s future growth.

The demand for computing power will continue to grow.

For those familiar with Moore’s Law, this law has supported the rapid growth of the semiconductor industry in the past five decades. In fact, the driving force of Moore’s Law is the increasing demand for computing power, and this demand will never disappear as long as the gap between the human brain and the “machine brain” still exists. The progress of AI technology is the best proof of this trend.

Currently, Nvidia’s GPUs dominate the computing field with a market share close to 90%. Although the demand for AI computing may not fully comply with Moore’s Law, the CEO of Meta Platforms has pointed out that AI systems need 10 times more computing resources than the existing computing power.

Hyperscale enterprises will continue the AI ARM race

The continuous growth of this computing power demand means that hyperscale enterprises will continue to invest and compete in the AI field. Microsoft recently announced that it will invest about $80 billion to build AI data centers to support the training of AI models. In addition, xAI deployed 100,000 Nvidia H200 GPUs in 19 days, further proving the shortage of GPUs.

New generation data centers

According to Nvidia’s CEO, they are building a data center the size of a house. It is expected that these data centers will become supercomputers and their computing power will exceed the sum of all existing data centers. As giant companies such as Amazon, Alphabet and Microsoft continue to increase their investment in data centers, we have reason to believe that the upgrading of data centers will provide strong market demand support for Nvidia.

The only problem is whether Nvidia can produce enough GPUs at a reasonable cost to meet this demand. Nvidia recently announced that it will launch a new generation of GPUs - GB300 and B300, and the launch of these products is only 6 months apart. It is reported that these new GPUs will provide significant performance improvements in inference and training models.

However, even so, the revenue growth forecast of Nvidia in the next 2 to 3 years is still lower than the average annual growth rate of 37% in the past five years, and we still need to pay attention to the balance between market demand and production capacity. Considering the current market demand and Nvidia’s production capacity, I think it is a reasonable and conservative forecast that the revenue growth rate in the next 5 years (until 2030) will exceed 30%.

Future Market Competition

In recent years, many investors have been anxious about the competition that Nvidia may encounter, especially from hyperscale enterprises such as Amazon (AMZN) and Google (GOOG).

Yes, these giants are indeed designing their own AI chips, mainly to reduce costs and optimize use cases, rather than to engage in the GPU business. If these companies really want to engage in the GPU business, they have to break the existing business model - Google no longer does search engines, and Amazon no longer sells things and turns to chip manufacturing? This sounds as unrealistic as asking Amazon to give up its delivery service and switch to running a restaurant.

These companies are smart enough to know in which areas to make money, and it is precisely because of this that they can become the “seven giants”.

Historically, it is common for hyperscale enterprises to design their own hardware to save money. Google has long had TPU, Tesla has also tried to design AI chips, and Amazon is also promoting AI inference hardware with lower cost and customized kernels. The problem is that these companies do not plan to take the GPU route. Only companies like Nvidia can launch the next generation of GPU products (such as GB300 and B300) within 6 months.

As for competitors, AMD is currently the second-largest player in the GPU market with a market share of about 10%. However, its market share is facing a decline, although its GPU revenue is still growing.

It is difficult for AMD to narrow the gap with Nvidia in the GPU market, and it will be very difficult to surpass Nvidia in the future. Even whether AMD can maintain its current position may face greater difficulties in the future.

Moat CUDA

What is Nvidia’s “moat”? It is their exclusive software for AI training integration - CUDA.

The efficiency of AI computing directly depends on software support. Although AMD has higher specifications in hardware (such as higher FLOPS/s), the actual AI computing efficiency is much slower than that of Nvidia. Obviously, AMD’s “software” is not yet able to meet the needs of efficient operation. Nvidia’s engineers work day and night and have put a lot of effort into updating new features, optimizing libraries and improving performance.

AMD’s CEO may need to work harder, but investing more in software and testing will directly increase their costs, which is not the news that Wall Street is willing to see. If AMD wants to compete with Nvidia in the GPU market, it has no choice but to have a cost advantage. The poor performance of AI training is due to the lack of vertical integration with network and data connection (exchange), and this problem is not easy to solve. After all, what users need is a plug-and-play experience, not just that the hardware can run.

The only technology that can defeat Nvidia now may be disruptive technologies such as quantum computing, or some chip technologies that we don’t know yet. These technologies may provide faster and more powerful computing power. However, it is estimated that it will take another ten or eight years to see the results of the commercial application of quantum computing. Don’t forget that it took more than 20 years for GPU technology to reach today’s height.

And do you know the only way to shake Nvidia? At present, the most likely is the antitrust action of the US government. Maybe it will be like what happened to “Bell Labs” or the splitting of Google. Whether the SEC thinks it is necessary to split Nvidia before its market cap reaches 10T? Only time can tell us the answer.

How is the current valuation?

In the past few years, Nvidia’s valuation has soared like a rocket. Many investors began to suspect: “Is this a bubble? Does its valuation really deserve this growth?” From the current situation, the competition seems to have calmed down - at least in the next few years, Nvidia is still that unreachable star.

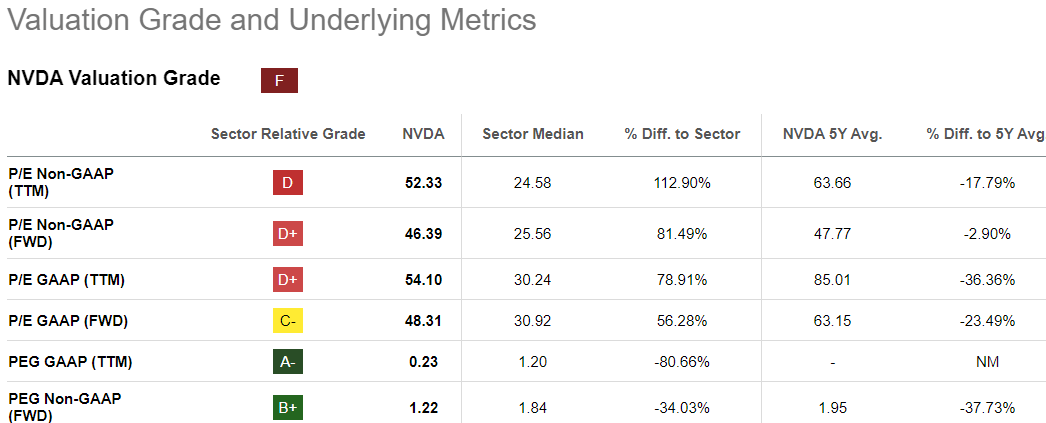

From the current market data, Nvidia’s price-to-earnings ratio is 24 times, and the expected compound annual growth rate (CAGR) is 20%. As a top growth company, this valuation is relatively low compared with its future growth potential. Although the expected price-to-earnings ratio in 2025 is 49 times, which may worry some investors, this shows that the market is full of confidence that Nvidia will achieve triple-digit growth in 2025 and the following years and more than 50% growth in 2026.

In fact, the market has not fully digested the expectation that Nvidia may expand at a growth rate of more than 20%.

By analyzing Nvidia’s valuation “discount”, we find that its PEG non-GAAP is 1.22, 34% lower than the industry median, which shows that its valuation is relatively cheap.

From the perspective of the traditional growth valuation method, this is simply an opportunity ignored by the market, indicating that the market has not given due recognition to the strongest growth and most profitable leading enterprise in the semiconductor industry. Do you think Nvidia will continue to dominate the semiconductor industry? I think the answer is yes - it is not only one of the fastest-growing companies, but also has strong profitability.

When Will It Reach Ten Trillion?

Regarding the possibility of Nvidia’s market cap exceeding $10 trillion, this may be divided into two stages.

In the first stage, assuming that the market sentiment improves, Nvidia’s stock price may rise rapidly in any bull market cycle. It is expected that the stock price will rise by 50% to $208, and the market cap will be close to $5 trillion.

In the second stage, if Nvidia can maintain its high-speed growth momentum, the stock price may double to $416, thus pushing the market cap to exceed $10 trillion.

Moreover, Broadcom (AVGO), as one of Nvidia’s peers, currently has a valuation close to Nvidia, but its profit growth forecast for the next two years is only half of Nvidia’s (30% vs. 111%, 20% vs. 50%). If the market really gives Nvidia a valuation similar to Broadcom’s, then the scenario of Nvidia’s market cap exceeding $10 trillion in 2026 is not impossible.

To sum up, I still think that Nvidia is the preferred long-term growth stock at present. Whether it will reach a market cap of $10 trillion in two or five years, I believe it may be the first technology company with a market cap exceeding $10 trillion.

Perfect Ending: Why NVDA is Still Worth Buying Strongly

Do you know? Computing power is the strongest and most persistent demand in human history, and Nvidia almost dominates in this “battle of computing power”. Don’t forget that it holds 90% of the GPU market share, and this market is experiencing a super explosion of AI.

Think about it, in the next decade, Nvidia’s leading position will be as stable as the Great Wall of Steel.

From an investment perspective, it is recommended to increase more NVDA stocks in 2025 as part of the investment portfolio. You may ask: “Why buy it? The stock price is so high.” But this is not only an expression of confidence in the company’s future growth potential, but also because of its continuous innovation in the fields of artificial intelligence and data processing, making Nvidia very likely to become the world’s first company with a market cap exceeding $10 trillion. With the soaring demand for AI and GPUs, Nvidia is about to usher in a “soaring” cycle, and the valuation cushion is also sufficient to prevent the stock price from falling suddenly.

Therefore, for investors seeking long-term growth and willing to bear certain market fluctuations, Nvidia is undoubtedly a high-quality asset worth holding. It can not only bring you rich returns in the next decade, but also is an existence that is definitely worth “heavy holding”. If you miss it, you will definitely regret it in the future.

*This article is provided for general information purposes and does not constitute legal, tax or other professional advice from BiyaPay or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional.

We make no representations, warranties or warranties, express or implied, as to the accuracy, completeness or timeliness of the contents of this publication.

Contact Us

Company and Team

BiyaPay Products

Customer Services

is a broker-dealer registered with the U.S. Securities and Exchange Commission (SEC) (No.: 802-127417), member of the Financial Industry Regulatory Authority (FINRA) (CRD: 325027), member of the Securities Investor Protection Corporation (SIPC), and regulated by FINRA and SEC.

registered with the US Financial Crimes Enforcement Network (FinCEN), as a Money Services Business (MSB), registration number: 31000218637349, and regulated by FinCEN.

registered as Financial Service Provider (FSP number: FSP1007221) in New Zealand, and is a member of the Financial Dispute Resolution Scheme, a New Zealand independent dispute resolution service provider.