- EasyCard

- Trade

- Help

- Announcement

- Academy

- SWIFT Code

- Iban Number

- Referral

- Customer Service

- Blog

- Creator

How to Use the US IBAN? Analysis of International Transfer Processes, Security, and SWIFT Codes

Image Source: unsplash

When conducting international remittances, you often encounter IBAN and SWIFT codes. IBAN is used to identify the recipient’s account, while SWIFT codes help identify the bank. You need to understand the difference between the two to successfully complete the international transfer process. Correctly filling in this information helps enhance the security of remittances and reduces errors. Please note that banks are very strict about verifying information, and any oversight may lead to transfer delays.

Key Points

- IBAN is mainly used in Europe and the Middle East to reduce errors in international transfers. The US does not use IBAN, requiring SWIFT codes and account numbers instead.

- SWIFT codes are unique identifiers for banks, ensuring funds are accurately transferred to the designated bank. You must verify them carefully to avoid errors.

- Before an international transfer, prepare the recipient’s information, bank details, and personal identification to ensure accuracy and minimize delays.

- Choose the appropriate transfer channel, understand each bank’s fees and processing times, and select the method that best suits your needs.

- During the transfer process, monitor the transfer status, keep transaction receipts, and contact bank customer service promptly if issues arise.

Introduction to US IBAN

What is IBAN?

When making international remittances, you often hear the term IBAN. IBAN, short for International Bank Account Number, is an international standard used to number bank accounts. IBAN is primarily used in European countries. Its structure includes a country code, check digits, bank identifier, and account number. You can use IBAN to accurately identify the recipient’s account, reducing transfer errors. The table below shows the differences in IBAN usage between the US and European countries:

| Country/Region | Uses IBAN |

|---|---|

| United States | No |

| European Countries | Yes |

IBAN makes international transfers in Europe safer and more efficient, but the US has not adopted this standard.

Role of IBAN in the US

When conducting international transfers in the US, you typically do not use IBAN. US banks prefer to use SWIFT codes and account numbers to identify recipients. The US does not have a standardized account identification system, unlike Europe and other regions. You should note that, although the US does not use IBAN, recipients in Europe or other IBAN-using countries may require you to provide an IBAN for remittances. The table below compares the main features of account identification in the US and other countries:

| Feature | United States | Other Countries |

|---|---|---|

| IBAN Usage | Not used | Used |

| Main Alternative | SWIFT Code | IBAN |

| Account Identification Standard | No standardized system | IBAN standardized system |

Difference Between IBAN and SWIFT

During the international transfer process, you often encounter IBAN and SWIFT codes. IBAN is used to identify specific bank accounts, while SWIFT codes are used to identify the bank itself. US banks primarily rely on SWIFT codes to complete international remittances. If you enter an incorrect SWIFT code, it may lead to transfer delays, rejections, or additional fees. Below are common consequences:

- Significant delays in bank processing of international transfers.

- If the SWIFT code is incorrect, the payment may be rejected.

- Banks may charge penalties for failed or returned transactions.

- Funds may be mistakenly transferred to another bank or account, with a complex and time-consuming recovery process.

When conducting international transfers in the US, you must verify the SWIFT code and recipient information to ensure the transfer is completed smoothly.

International Transfer Process

Image Source: unsplash

When conducting international transfers through US banks, you need to follow a standard process. Mastering the international transfer process can help you reduce errors and enhance fund security. Below, I will explain the entire process step by step.

Pre-Transfer Preparation

Before starting an international transfer, you must prepare all necessary documents. Thorough preparation can make the international transfer process smoother. You need to collect the following information:

- Recipient details, including name, address, and country.

- Recipient’s bank information, such as SWIFT/BIC code and IBAN number (if the recipient’s bank is in Europe or other IBAN countries).

- Your US bank account number.

- Government-issued identification and proof of address.

- Social Security Number (SSN).

- Proof of fund source (may be required for large transfers).

- Reason for the transfer, amount, and desired currency type.

Tip: You should confirm all information with the recipient in advance to avoid transfer failures or delays due to incorrect details.

Filling in Account Information

When filling in account information, you must carefully verify each item. The accuracy of account information is critical in the international transfer process. Common errors include unverified recipient information, number confusion, and failure to check details carefully. You can follow these steps:

- Collect the recipient’s full name, bank name, address, and account number.

- Correctly enter the SWIFT code and IBAN number (if applicable).

- Input the transfer amount and currency, and confirm any additional fees.

- Carefully review all entered information to ensure accuracy.

Note: An incorrect account number or bank code may lead to fund loss or delays. You should double-check all details.

Choosing a Transfer Channel

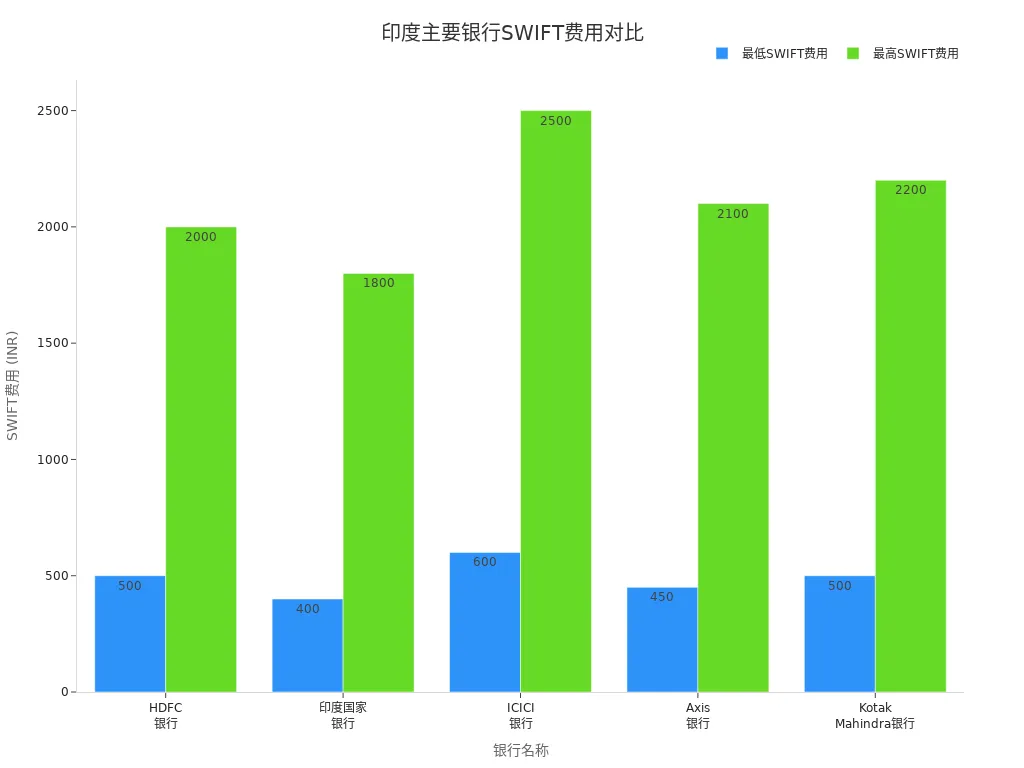

You can choose from multiple channels to complete an international transfer. Different banks and channels vary in fees, speed, and services. You should select the most suitable method based on your needs. The table below shows international transfer fees for major US banks (in USD):

| Bank | Incoming Fee | Outgoing Fee |

|---|---|---|

| Bank of America | $16 | $35 |

| Capital One | $0-$15 | $40 |

| Charles Schwab | $0 | $15 |

| JPMorgan Chase | $15 | $5 (foreign currency)/$40 (USD) |

| Citibank | $15 | $0 (foreign currency)/$35 (USD) |

| Discover Bank | $0 | $30 |

| HSBC | $0 | $0 |

| Huntington Bank | $15 | $75 |

| Navy Federal | $0 | $25 |

| PNC Bank | $15 | $5 (foreign currency)/$40 (USD) |

| Regions Bank | $18 | $45 |

| TD Bank | $15 | $50 |

| Truist Bank | $20 | $65 |

| USAA | $0 | $20-$25 |

| Wells Fargo | $15 | $0 (foreign currency)/$25+ |

You can initiate international transfers through bank counters, online banking, or third-party payment platforms. You should understand the fees and processing times of each channel in advance. Generally, when using SWIFT codes for international transfers, banks charge a 3%-5% exchange rate fee. When using IBAN, processing fees and commissions vary by country.

Submission and Tracking

After completing all information, you can formally submit the international transfer request. The international transfer process typically follows these steps:

- Visit a local US bank branch or log into online banking.

- Submit all collected information, including recipient account, SWIFT code, IBAN number, etc.

- The bank will generate a federal reference number as a transaction receipt.

- You can track the transfer status through bank customer service, branches, or online banking. Some banks support SWIFT tracking.

- If you are the recipient, communicate with the sender to obtain the reference number and confirm transfer progress.

The average processing time for international transfers is 1 to 5 business days. If you submit the request before the bank’s cutoff time, it may be processed the same day. Transfers may go through intermediary banks, and the recipient bank may require an additional 1 to 2 days for processing.

Reminder: You should keep all transaction receipts and reference numbers for future inquiries and tracking.

As long as you follow the steps above, the international transfer process will be clear and efficient. You should prioritize verifying information at every step to ensure funds reach the recipient’s account safely.

SWIFT Code Analysis

What is a SWIFT Code?

When conducting international transfers, you frequently encounter SWIFT codes. A SWIFT code is a standardized bank identifier used for information exchange between global banks. You can use a SWIFT code to accurately identify each bank. SWIFT codes typically consist of 8 to 11 characters in the format AAAA BB CC DDD. The first four characters represent the bank code, the next two are the country code, followed by two for the location code, and the last three are the branch code (optional). For example, a major US bank’s SWIFT code might be BOFAUS3N.

The table below shows the definition of SWIFT codes and their global adoption rate:

| Definition | Global Adoption Rate |

|---|---|

| SWIFT codes are a standardized messaging system for international money transfers via the SWIFT network. | As of 2018, approximately half of high-value cross-border payments globally use the SWIFT network. |

Role of SWIFT Codes

When conducting international remittances, SWIFT codes play a critical role. The SWIFT network does not directly transfer funds but sends payment instructions between banks via SWIFT codes, enabling fast, accurate, and secure international fund transfers.

SWIFT codes are indispensable tools in international transactions, ensuring funds are transferred safely and accurately. Without SWIFT codes, the risk of erroneous transfers increases significantly, potentially leading to delays and financial losses.

You can understand the specific roles of SWIFT codes through the following points:

- SWIFT codes serve as unique identifiers for banks, ensuring funds are correctly routed.

- They are critical in international banking, ensuring funds are transferred to the correct institution.

- SWIFT codes facilitate seamless communication between banks, reducing the risk of transaction errors.

How to Find and Enter SWIFT Codes

When filling in international transfer information, you must accurately enter the SWIFT code. You can find a US bank’s SWIFT code through the following methods:

- Check bank statements: Bank statements typically display the SWIFT code in the account information section.

- Online banking portal: Online banking portals also provide SWIFT codes in the account information or “international transfer” or “wire transfer” sections.

- Contact the bank directly: Call the bank branch to obtain the SWIFT code.

- Use the SWIFT official website: Use SWIFT’s online search tool to find SWIFT codes.

- Third-party tools: Online resources like bank.codes can help find SWIFT codes, but always verify with the bank before sending funds.

When entering SWIFT codes, you should also watch out for these common errors:

- Input Errors: Entering an 8- to 11-character code, especially in a rush, can easily lead to minor mistakes. A single incorrect letter or number can invalidate the entire code.

- Incorrect Format: SWIFT codes must be entered as a single string without spaces or special characters. A common error is adding spaces within the code. If spaces are included, the bank may reject your transfer.

- Incorrect Recipient Information: SWIFT codes are specific to banks, but funds also need to reach the correct person or company. You need the correct SWIFT/BIC code and recipient bank information. If these details are incorrect, even if the SWIFT code is accurate, your transfer may be rejected.

As long as you carefully verify the SWIFT code and recipient information, you can significantly reduce the risk of errors in international transfers.

Security and Risk Prevention

Image Source: unsplash

Security Measures

When conducting international transfers in the US, banks employ various technological measures to ensure fund security. Bank systems use encryption to protect the transmission of sensitive information. Encryption prevents unauthorized access and data breaches, ensuring your payment data is not obtained by cybercriminals. The SWIFT system also integrates identity verification and strict access controls to further enhance security.

US banks typically require two-factor authentication. You need to generate a code using a secure device to log into online banking. When adding a recipient for the first time, the system will require an additional code for setup. During the transfer, you must complete a transaction verification step. The table below shows the common two-factor authentication process:

| Step | Description |

|---|---|

| 1 | Use a secure device to generate a code to log into online banking. |

| 2 | For the first payment, generate an additional code to set up a new recipient. |

| 3 | During the transaction, generate a verification code to complete the transfer. |

Common Risks

During the international transfer process, you may encounter some security risks. SWIFT transfers have high fees and longer processing times, typically taking 1 to 3 business days. You may also face the following risks:

- Irreversibility: Once funds are sent via wire transfer, recovering them is very difficult. If you enter incorrect recipient information or fall victim to a scam, funds are usually unrecoverable.

- Fraud Vulnerability: Scammers may induce you to make wire transfers or attempt to compromise your account for unauthorized transfers. Lack of transaction protection makes it hard to recover lost funds.

- Exchange Rate Risk: International transfers involve currency exchange, and exchange rate fluctuations may affect the amount the recipient actually receives.

You should understand these risks and take preventive measures to avoid unnecessary losses.

Prevention Tips

You can take several measures to reduce international transfer risks. US financial institutions recommend keeping detailed records of each wire transfer process, including steps for handling exceptions and emergencies. You should regularly review and update relevant policies to ensure the process remains safe and effective.

When sharing sensitive information, use encrypted emails or secure portals and avoid public email accounts. You can also establish a vendor management program with multi-step verification for any changes to payment information. Team members should receive regular security training and simulate fraud scenarios to enhance prevention capabilities.

Banks provide security features, and you can work with them to enable additional safeguards. You should also set up monitoring and auditing processes to detect unusual transactions promptly.

Before submitting an international transfer, you need to verify the recipient bank’s routing number, account number, SWIFT/BIC code, and IBAN. Some countries may also require the purpose of payment and special codes.

By carefully verifying all information and choosing legitimate channels, you can effectively reduce the security risks of international transfers.

In the international transfer process, you must understand the core roles of IBAN and SWIFT codes. SWIFT codes help you identify the target bank, while IBAN is used to pinpoint specific accounts, especially in regions like Europe and the Middle East. US banks typically require you to provide account numbers, routing numbers, and SWIFT codes. You should keep the following points in mind:

- IBAN is mainly used in Europe, the Middle East, and some Caribbean regions, reducing errors and speeding up cross-border transactions.

- SWIFT codes ensure funds reach the designated bank accurately.

- When transferring to countries that do not use IBAN, other methods are needed to identify banks and accounts.

- Before transferring, carefully verify all information and monitor the transfer status, and contact bank support promptly if issues arise.

As long as you prioritize information verification and risk prevention, you can significantly improve the security and success rate of international transfers. If you have questions, consult professional institutions or refer to relevant resources to ensure every step is accurate.

FAQ

Why Don’t US Banks Use IBAN?

When handling international remittances with US banks, you are not required to provide an IBAN. The US uses SWIFT codes and account numbers to identify accounts. IBAN is mainly used in Europe and the Middle East, and the US lacks a unified standard.

You need to choose the correct account identification method based on the recipient’s country.

How to Find a US Bank’s SWIFT Code?

You can log into online banking and check the international transfer page. You can also call the bank’s customer service for assistance. The SWIFT official website and third-party tools can help you find SWIFT codes, but final verification is recommended.

| Method | Description |

|---|---|

| Online Banking | Account information page |

| Customer Service | Direct inquiry |

| SWIFT Website | Online search tool |

How Long Does an International Transfer Take?

After submitting an international transfer, funds typically arrive within 1 to 5 business days. Processing time depends on the bank, channel, and intermediary banks. You can track progress using the reference number.

You should keep transaction receipts for inquiries and verification.

What to Do If a Transfer Fails?

If you encounter a transfer failure, contact bank customer service immediately. You need to verify account information, SWIFT codes, and fund sources. The bank will help identify the issue and process a refund or resend the transfer.

- You should prepare all transaction receipts and reference numbers.

- You can request a detailed processing report from the bank.

Which International Transfer Channels Do US Banks Support?

You can choose from bank counters, wire transfers, online banking, or third-party payment platforms. Fees and speeds vary by channel. You should select the appropriate channel based on the amount, destination, and urgency.

You can consult the bank in advance to understand the specific requirements and fees for each channel.

Navigating international transfers to the US can be daunting, with intricate data entry, steep fees, exchange rate volatility, and fraud risks turning seamless remittances into a chore. Imagine a platform offering a total fee as low as 0.5% (covering the full process), real-time rate checks, seamless swaps between 30+ fiat currencies and 200+ digital assets, global coverage, and same-day delivery. How would that transform your experience?

BiyaPay is built to solve these issues. As a cutting-edge digital finance platform, we streamline mobile-based transfers, letting you input SWIFT codes and account details effortlessly for swift US remittances. Use our real-time exchange rates to secure mid-market pricing and avoid hidden markups. With multi-layer encryption, FinCEN compliance, and two-factor authentication, BiyaPay ensures secure, trackable transactions. Sign up in minutes to handle everything from daily transfers to large remittances with ease.

Say goodbye to remittance hassles! Visit BiyaPay now to explore live rates and optimize your transfer. Sign up for a BiyaPay account today and unlock low-cost, instant, and secure US transfers, making cross-border support effortless and reliable.

*This article is provided for general information purposes and does not constitute legal, tax or other professional advice from BiyaPay or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional.

We make no representations, warranties or warranties, express or implied, as to the accuracy, completeness or timeliness of the contents of this publication.

Contact Us

Company and Team

BiyaPay Products

Customer Services

is a broker-dealer registered with the U.S. Securities and Exchange Commission (SEC) (No.: 802-127417), member of the Financial Industry Regulatory Authority (FINRA) (CRD: 325027), member of the Securities Investor Protection Corporation (SIPC), and regulated by FINRA and SEC.

registered with the US Financial Crimes Enforcement Network (FinCEN), as a Money Services Business (MSB), registration number: 31000218637349, and regulated by FinCEN.

registered as Financial Service Provider (FSP number: FSP1007221) in New Zealand, and is a member of the Financial Dispute Resolution Scheme, a New Zealand independent dispute resolution service provider.